Investment Outlook: Third Quarter 2020: How Will the 2020 Election Impact the Stock Market?

How Will the 2020 Election Impact the Stock Market?

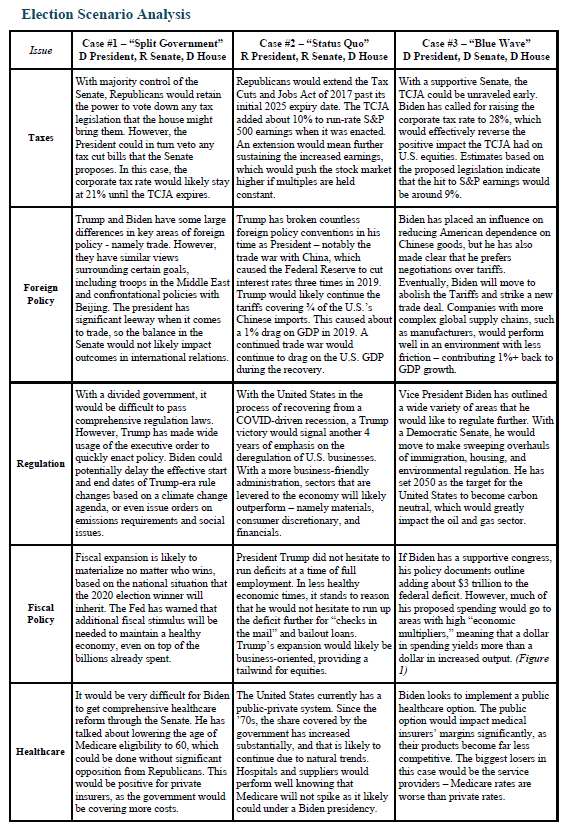

In the volatile year of 2020, investors are faced with two highly polarized outcomes following election day in November. Options markets are pricing in significantly higher volatility in the months surrounding the election, as the two candidates have vastly different policies they aim to implement. The direction of the Senate majority also has an impact – in a split government scenario, laws from either side are much more difficult to pass. Given the population bias in electing the House, it will likely stay with the Democrats. The Senate has a bias to the Republicans – but with 23 of the Republicans’ 53 seats up for reelection, that too could change. The analysis on the back of this page lays out 3 likely election outcomes and investigates the most important issues relating to the stock market in each case.

A Blue Wave

Among all points to be addressed should the Democrats win the Presidency, the Senate, and the House, the headline tax-rate increase impacts the broad U.S. stock market the most. However, easier fiscal policy and a larger budget deficit than either of the other scenarios should provide a balancing reaction. The market is already pricing a slightly higher chance of a Biden victory in light of the polls. With more expansionary Democratic fiscal policy, cyclical sectors like industrials and materials will likely outperform over defensive sectors like consumer staples and utilities. Some of the more tax-impacted sectors, such as financials and pharmaceuticals, are also under threat of new regulation and will likely experience selling in the event of a Biden victory.

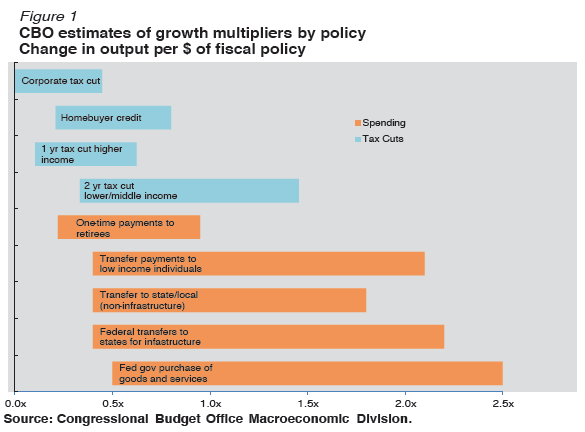

Presuming that the filibuster is not removed, even in a Democratic majority, 60 votes would still be needed in the Senate to pass most legislation. This means that some form of moderate consensus would have to be reached and could likely result in a Democratic Senate focusing on passing a handful of key issues in 2021. The exception would be budgetary issues that could pass via the reconciliation process. This could be used to pass many elements of a stimulus package, for example, and has historically been used to pass healthcare and tax legislation (e.g. the Affordable Care Act and the 2017 tax reform law). This means that Biden’s policies in healthcare and tax are more likely to be passed in a Blue Wave, whereas the regulatory proposals and infrastructure programs would be whittled down in size before they reach a 60-vote majority.

The Output Gap and Interest Rates Under Biden

The output gap measures the difference between the actual and maximum potential output of an economy expressed as a percent of GDP. Employment is a key component of potential output – if only 88% of the workforce is employed, then there is room for more output. With a positive output gap, there is a higher demand for goods and services than is conventionally available. This means that businesses are pushed beyond their maximum efficiency, and are effectively supply bound. When there is more demand than supply, inflation is spurned as labor and materials costs increase in response to the increase in demand.

With a unified Democratic government, the deficit could increase by about $3 trillion. The output gap would increase notably, bringing the core PCE inflation number above the 2.1% threshold for Fed intervention by 2023. If employment recovers to a reasonable maximum, Biden’s policies would bring a rate increase forward, taking effect in 2023 instead of the widely forecasted 2025. Biden’s proposed increases in government spending and transfer payments to aid in the recovery all enable this to take effect.

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, Beese Fulmer Private Wealth Management ("Beese Fulmer") makes no representation or warranty as to the accuracy or completeness of the information, which should not be used as the basis of any investment decision. Information contained on third-party websites that Beese Fulmer may link to is not reviewed in their entirety for accuracy and Beese Fulmer assumes no liability for the information contained on these websites. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from Beese Fulmer. For more information about Beese Fulmer, including our Form ADV brochures, please visit https://adviserinfo.sec.gov and search for our firm name.